Understanding Why Formation Is Your Most Important First Step

Before you make your first sale, hire your first employee, or sign your first contract, you need to make a decision that will shape everything that follows: how to legally form your business. This single decision determines how your income is taxed, whether your personal assets are protected from business liabilities, how easily you can bring in investors or partners, and how your business is perceived by banks, clients, and government agencies.

Many first-time entrepreneurs skip this step or delay it, operating informally while they test their idea. While this may seem practical in the short term, it carries serious risks. Without formal registration, you have no legal separation between yourself and your business. This means if your business is sued, a creditor can come after your personal bank accounts, home, car, and savings. It also means you cannot open a proper business bank account, cannot legally enter into enforceable contracts under a business name, and cannot apply for most forms of business funding or government assistance.

Formal company formation is not just a legal formality it is the act of making your business real, legitimate, and protected. It signals to the world that you are serious, professional, and committed to operating responsibly. Done correctly from the start, it saves you enormous time, money, and stress down the road and positions your business for sustainable, scalable growth.

Selecting the Right Legal Structure for Your Business

The legal structure you choose for your business is the architectural blueprint of your company. It dictates your tax obligations, your personal liability exposure, your ability to raise capital, and how decisions are made within the organization. Choosing the wrong structure early or failing to revisit it as your business evolves can result in overpaying taxes, personal financial exposure, or costly and time-consuming restructuring down the line.

A Sole Proprietorship is the most basic form of business the owner and the business are legally the same entity. There is no registration process, no separation of personal and business liability, and income is taxed directly on the owner’s personal tax return. While simple to set up, it offers no protection whatsoever. If the business is sued or cannot pay its debts, creditors can pursue the owner’s personal assets without restriction.

A General Partnership operates similarly but involves two or more people sharing ownership, profits, and critically unlimited personal liability. Even if only one partner makes a bad decision, all partners can be held personally responsible for the consequences. For this reason, most legal and business advisors strongly recommend formalizing any multi-owner business as an LLC or corporation rather than a general partnership.

A Limited Liability Company (LLC) is the most widely chosen structure for small and mid-sized businesses, and for good reason. It combines the simplicity and tax flexibility of a sole proprietorship or partnership with the liability protection of a corporation. LLC members are not personally liable for business debts or legal judgments, and the business can elect to be taxed in several different ways depending on what is most advantageous. LLCs also have fewer administrative requirements than corporations, making them easier to manage for smaller teams.

The Company Registration Process A Step-by-Step Walkthrough

Once you have decided on your legal structure, the next phase is registration transforming your business idea into a legally recognized entity. The process involves several interconnected steps, and completing them in the right order ensures your business is fully legitimate, properly documented, and ready to operate.

Begin with your business name. Choose a name that is distinctive, memorable, and legally available. Conduct a name availability search through your state’s Secretary of State database to confirm no existing business is already registered under that name. Simultaneously, search the United States Patent and Trademark Office (USPTO) Trademark Electronic Search System (TESS) to check for federally registered trademarks. Also verify that a matching or closely similar domain name is available online in today’s digital-first business environment, your web presence matters from day one.

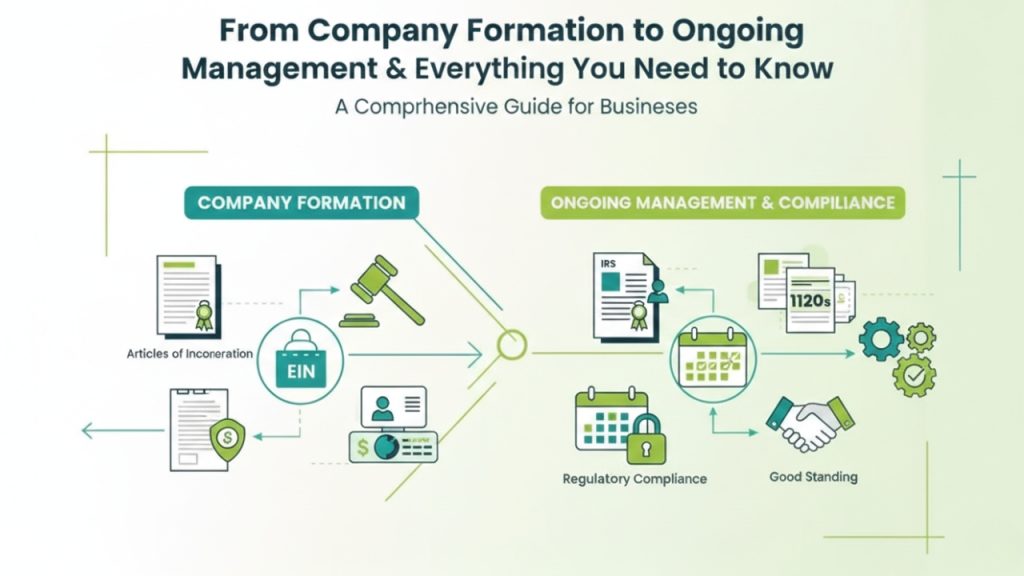

Next, file your formation documents with the appropriate state authority typically the Secretary of State’s office. LLCs file Articles of Organization. Corporations file Articles of Incorporation. These documents establish your company’s legal existence and typically include the business name and address, the name and address of your registered agent, the names of founding members or directors, and the purpose of the business. Filing fees vary by state, ranging from as low as $50 to several hundred dollars.

After filing, obtain your Employer Identification Number (EIN) from the Internal Revenue Service. The EIN is your business’s federal tax identification number the equivalent of a Social Security number for your company. It is required for opening business bank accounts, applying for business loans, hiring employees, and filing federal tax returns. The process is free and can be completed online through the IRS website in minutes.

Building the Management Foundation Your Business Needs

With your business legally formed and registered, the next critical challenge is establishing the management infrastructure that will allow it to operate effectively, make sound decisions, resolve conflicts constructively, and grow without losing control. This is where many businesses falter not because the founders lack vision or talent, but because they underestimate how much structure and process a growing organization requires.

Every LLC should have a comprehensive Operating Agreement, and every corporation should have detailed Corporate Bylaws. These are not just formalities they are the rulebook for how your company operates. An Operating Agreement for an LLC should clearly define each member’s ownership percentage and capital contribution, voting rights and decision-making thresholds (i.e., what percentage of ownership is required to approve different types of decisions), how profits and losses are allocated and when distributions are made, what happens when a member wants to leave or sell their interest, and how disputes between members are resolved. Without this document, your state’s default LLC rules apply which may not reflect your intentions at all.

Corporate Bylaws serve a similar function for corporations, establishing rules for board composition and elections, officer roles and responsibilities, how shareholder meetings are conducted, how shares are issued and transferred, and how the corporation can be amended, merged, or dissolved. Regular board meetings or member meetings held at least annually and documented with formal minutes are required by law in many states and demonstrate the kind of good corporate governance that protects owners from personal liability.

Hiring, Managing, and Retaining the Right People

A business is only as strong as the people behind it. As you move from solo founder to team leader, the decisions you make about who to hire, how to onboard them, and how to manage and retain them will have a profound impact on your company’s culture, productivity, and long-term success. Poor hiring decisions are expensive studies estimate that the cost of a bad hire can range from 30 percent to 150 percent of that employee’s annual salary when you account for recruitment costs, training time, lost productivity, and the disruption to team morale.

Start by defining each role clearly before you begin recruiting. Write detailed job descriptions that outline specific responsibilities, required qualifications, and the metrics by which performance will be measured. During the hiring process, evaluate not just technical skills and experience, but cultural fit how a candidate’s values, work style, and communication approach align with the environment you are building. A technically brilliant hire who undermines team cohesion or disregards company values will ultimately cost you more than their salary.

Once hired, onboard new team members thoughtfully. Provide clear training, introduce them to the team and company culture, set expectations in writing, and check in regularly during their first 90 days. Employment law compliance is non-negotiable from the moment you hire your first employee. Properly classify all workers as either employees or independent contractors misclassification is one of the most common and costly employment law violations, triggering back taxes, penalties, and lawsuits. Maintain signed offer letters, employment contracts, employee handbooks, and I-9 verification documents for every hire.

Navigating Compliance Federal, State, and Industry-Specific

Compliance is not a destination it is a continuous journey that evolves as your business grows, expands into new markets, hires more employees, and operates in a changing regulatory environment. Many business owners view compliance as a burden, but the cost of non-compliance in fines, penalties, legal fees, reputational damage, and lost business far exceeds the cost of staying current. A proactive approach to compliance is not just legally necessary; it is a competitive advantage.

At the federal level, businesses must comply with IRS requirements for income tax, payroll tax (including federal income tax withholding, Social Security, Medicare, and federal unemployment tax), and potentially excise taxes depending on the industry. The IRS requires payroll taxes to be deposited on a schedule determined by the size of your payroll failure to deposit on time results in escalating penalties. Businesses with employees must also comply with the Fair Labor Standards Act governing minimum wage and overtime, the Occupational Safety and Health Act ensuring safe working conditions, the Equal Employment Opportunity laws prohibiting discrimination, the Americans with Disabilities Act requiring reasonable accommodations, and the Family and Medical Leave Act providing eligible employees with job-protected leave.

At the state level, most businesses must file annual or biennial reports with their Secretary of State to maintain good standing. These reports confirm your registered agent, business address, and ownership information. Missing these deadlines can result in late fees and, in many states, administrative dissolution your business is legally terminated without your knowledge or consent. States also impose their own income taxes, sales taxes, unemployment insurance requirements, and industry-specific regulations that must be monitored and followed.

Intellectual Property Protection Securing What You Have Built

In an increasingly knowledge-based economy, your intellectual property is often worth more than your physical assets. Your brand, your innovations, your creative content, your proprietary processes, and your customer relationships represent years of investment, creativity, and competitive positioning. Protecting them is not optional it is a fundamental business responsibility.

Trademark protection secures your brand identity your business name, logo, slogans, product names, and any other identifiers that distinguish your business in the marketplace. Register your trademarks with the USPTO as early as possible. Federal trademark registration provides nationwide protection, legal presumption of ownership, the right to use the ® symbol, and the ability to stop importation of infringing foreign goods through U.S. Customs. Without registration, your rights are limited to the geographic area where you actively use the mark, leaving you vulnerable to a competitor who registers a similar mark in another region.

Copyright protection covers original creative works articles, website content, marketing materials, software code, photographs, videos, music, and artistic designs. Copyright protection arises automatically when an original work is created, but registering with the U.S. Copyright Office significantly strengthens your legal position. Registered copyrights can support claims for statutory damages and attorney’s fees in infringement lawsuits, whereas unregistered works can only recover actual damages which are often difficult to prove and may be minimal.

Risk Management and Business Insurance

Every business, no matter how carefully managed, faces risks. Equipment breaks down. Employees are injured. Clients allege professional negligence. Customers are harmed by products. Data is breached. Natural disasters strike. A competitor files a frivolous lawsuit. These events can and do happen to well-run businesses and without the right insurance coverage, a single major incident can wipe out years of hard work and financial progress in a matter of months.

General Liability Insurance is the cornerstone of any business insurance program. It covers third-party claims for bodily injury, property damage, and personal and advertising injury for example, if a customer slips and falls at your location, or if your advertising allegedly infringes on a competitor’s copyright. Most commercial leases, client contracts, and business license applications require proof of general liability coverage. Professional Liability Insurance, also known as Errors and Omissions (E&O) insurance, covers claims that your professional advice or services caused financial harm to a client. This coverage is essential for consultants, accountants, attorneys, architects, engineers, IT professionals, and anyone else who provides advice or specialized services for compensation.

Financial Controls, Record Keeping, and Corporate Governance

Strong financial controls and meticulous record-keeping are the backbone of a well-governed business. They protect you legally, enable sound decision-making, simplify tax compliance, and are absolutely essential when the time comes to raise investment, secure a loan, or sell the business. Investors and acquirers conduct thorough due diligence and businesses that cannot produce clean, organized, accurate financial and corporate records immediately raise red flags that can kill deals or dramatically reduce valuations.

Implement internal financial controls that prevent fraud, errors, and misappropriation of funds. Segregate financial duties the person who approves expenses should not be the same person who processes payments. Require dual authorization for transactions above a certain dollar threshold. Conduct regular bank reconciliations to ensure your accounting records match your actual bank balances. Perform periodic internal audits to verify that your financial processes are functioning as designed and that no irregularities exist. As your business grows, consider engaging an external auditor annually to provide an independent assessment of your financial statements.

Corporate record-keeping requirements vary by state but generally include maintaining a register of all shareholders or LLC members and their ownership interests, minutes from all board of directors or member meetings held, records of all major business decisions and resolutions, copies of all formation documents, operating agreements or bylaws, and any amendments thereto, all signed contracts, leases, and material business agreements, complete financial records including bank statements, invoices, receipts, payroll records, and tax returns, and personnel files for every current and former employee. Federal law requires retention of most tax records for at least seven years. Implement a digital document management system Google Workspace, Microsoft SharePoint, or a dedicated legal document platform to ensure records are stored securely, organized logically, backed up redundantly, and accessible to authorized personnel from anywhere.

Strategic Growth Planning and Business Scalability

A business without a growth strategy is just surviving not thriving. Strategic planning is the process of deliberately defining where you want your business to go, identifying the resources and capabilities you need to get there, and putting a concrete roadmap in place to close the gap between where you are today and where you want to be. Without this intentionality, businesses tend to react to circumstances rather than shape them, leaving growth to chance rather than strategy.

Conduct an annual strategic review that examines your market position, competitive landscape, financial performance, operational capacity, and the strength of your team. Identify your core competitive advantages what your business does better than anyone else and ensure your strategy amplifies and protects those strengths. Set specific, measurable annual goals broken down by quarter, and review progress against those goals monthly. Establish key performance indicators (KPIs) for every department sales, marketing, operations, finance, and customer service so that performance is measured objectively and continuously improved.

As your business grows, your legal and financial structure may need to evolve. A business that started as a single-member LLC may need to add members, restructure equity, create subsidiary companies, or convert to a corporation to accommodate growth, investment, or international expansion. Engage your business attorney and CPA in your strategic planning process not just at tax time, but as ongoing strategic advisors who can identify legal and financial risks and opportunities before they become problems or missed opportunities. Build scalable systems and processes from the beginning document how every core function of your business operates so that growth does not require rebuilding everything from scratch.

Exit Planning and Business Succession

Every business owner will eventually exit their business whether through a sale, a transfer to family, a management buyout, a merger, an IPO, or simply closing the doors. The difference between a rewarding exit and a painful one almost always comes down to how much planning was done years in advance. Business owners who begin thinking about their exit strategy early well before they intend to act on it consistently achieve better financial outcomes, smoother transitions, and greater personal satisfaction.

If your goal is to sell the business, begin preparing years in advance. Buyers and their advisors will conduct exhaustive due diligence examining your financials, contracts, customer relationships, employee arrangements, intellectual property portfolio, compliance history, and legal records. Businesses with clean, well-organized records; consistent revenue growth; strong management teams that are not dependent on the founder; and documented, repeatable processes command premium valuations. Businesses that have been run informally, with poor records and owner-dependent operations, often sell at a significant discount or fail to attract serious buyers at all.

Final Thoughts

From the moment you decide to start a business to the day you eventually transition out of it, every decision you make about formation, management, compliance, and governance shapes the trajectory of everything you build. The entrepreneurs who achieve lasting success are not necessarily the ones with the best ideas or the most charisma they are the ones who take the time to build their businesses on solid legal and operational foundations, who invest in professional management systems, who treat compliance as a strategic discipline rather than a bureaucratic burden, and who plan intentionally for growth and transition.

The path from company formation to ongoing management and compliance is not always simple or straightforward. There will be challenges, unexpected regulatory requirements, difficult personnel decisions, and moments when the administrative demands of running a business feel overwhelming. But every step you take to build a properly structured, well-managed, and legally compliant business is an investment in your financial security, in the livelihoods of the people who work for you, in the trust of the customers and partners who depend on you, and in the long-term value of the enterprise you are creating.

Surround yourself with exceptional advisors a skilled business attorney who understands your industry, a sharp and proactive CPA who thinks strategically about your financial future, a knowledgeable insurance broker who ensures you are comprehensively protected, and mentors who have walked this road before and can share hard-won wisdom. Leverage technology to automate compliance tracking, financial reporting, and document management. Build a culture of accountability, transparency, and continuous improvement from day one. And never stop learning — the regulatory environment, tax laws, employment standards, and best management practices all evolve, and staying informed is a competitive advantage in itself.